It’s fair to say I’m not the world’s most patient person. My inner voice is constantly telling me “Not far enough! Not fast enough!” And indeed, our industry has seen real progress, but there is always more to do.

Our deeply-embedded mind-set has been to manufacture products and then find consumers to sell them to, rather than focusing on our customers and their wants and needs. But this is going to change.

I’m referring, of course, to the regulator’s Consumer Duty of Care. With the final rules published this week, implementation is due to take effect in April 2023 (or possibly later in the year if delayed), there are concerns over what additional burden regulated product providers will be required to shoulder. What we do know is that Consumer Duty will put big, expensive and, let’s be honest, pretty alarming responsibilities on any financial services business.

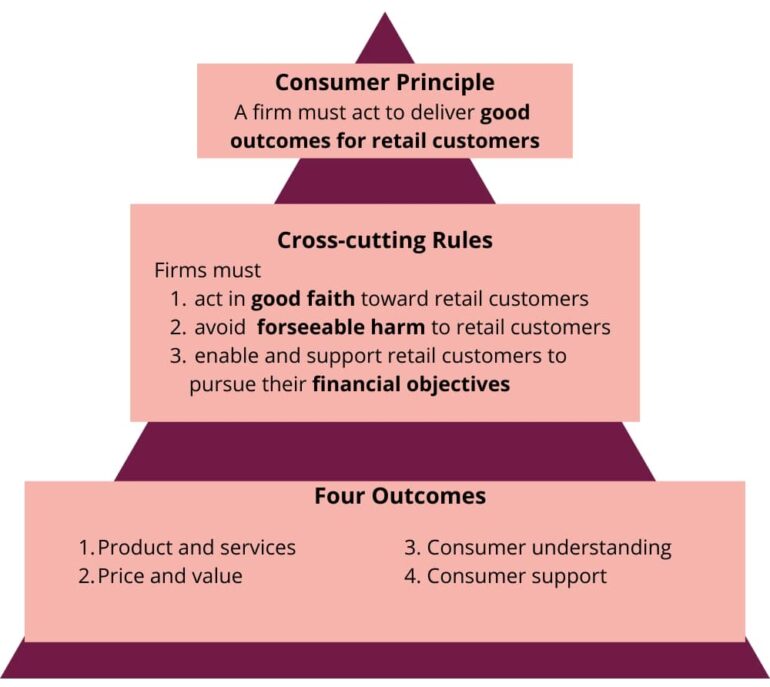

The new Principle 12 states that “A firm must act to deliver good outcomes for retail consumers.” No hiding places. No buck-passing. No closing the sale and walking away. If you serve the retail market, you must act to deliver good outcomes.

I simply cannot see how firms can meet their new Consumer Duty obligations without building their customer relationships around Open Finance and more broadly Open Data. In the old, soon-to-be-departing, product-centric world, it has been sufficient for firms to relate to customers purely in terms of the product/s they’ve sold to them.

But a customer-centric view of the world means taking a genuinely holistic view of your customers’ finances.

The kind of data insights necessary to recognise and meet customers’ needs – and to keep meeting customers’ needs over the lifetime of a contract – can only be derived from a platform that aggregates the customer’s financial position, and automates the analysis for both the consumer and the provider. Thereby positioning the right products and services to the right people at the right time to achieve better outcomes across their entire financial life.

This represents a 180-degree shift of responsibility. he onus is now on providers to tell their customers when they have something better or more suitable in their portfolio – and invite them to make the switch if they choose to do so.

Let’s take one of the most simple and straightforward examples. If a borrower’s life was going well and the Loan to Value (LTV) ratio on their mortgage changed so that they became eligible for a better interest rate, a lender should, under Consumer Duty, alert them to a more suitable product immediately.

Providing the data-driven insights that can underpin individual, personalised propositions like this is at the heart of what Moneyhub does. And we can provide them either directly to the customer or, with the customer’s permission, to firms providing products and services, so they can create tailored communications and propositions to meet individual customers’ proven needs.

Moving towards an Open Finance-based, data-driven, customer-centric model is wonderfully, transformationally good for business, good for profitability, and good for efficiency.

We’ve come a fairly long way, but there’s a long way still to go – and the next leap forwards is the move to aggregating individual customers’ data, from banking and pensions to loans, investments, mortgages and properties, and making use of the insights it just can’t stop providing.

Consumer Duty certainly presents an alarming array of demands and challenges, but it also presents an even broader array of fabulous opportunities, and these need to be embraced.

So, my plea to the industry is to take this seriously, let legacy thinking be legacy and consider how you can take this regulation and turn it into a real opportunity for your business and your customers. The results will be truly fantastic when the hidden value in your customers data is unlocked to achieve better outcomes for all.

Samantha Seaton is CEO of Moneyhub