House prices continued to increase in July, albeit at a slower pace in monthly terms, figures from Nationwide show.

Nationwide’s House Price Index for revealed that house prices were up 0.1% on June, when they rose by 0.2%.

On an annual basis prices were 11.0% higher, up from 10.7% in June. As such the average price of a home in the UK now stands at £271,613.

Robert Gardner, Nationwide’s chief economist, said: “July saw a modest increase in the rate of annual house price growth to 11.0%, from 10.7% in June. Prices rose by 0.1% month-on-month, after taking account of seasonal effects – the twelfth successive monthly increase, which kept annual price growth in double digits for the ninth month in a row.

“The housing market has retained a surprising degree of momentum given the mounting pressures on household budgets from high inflation, which has already driven consumer confidence to all-time lows. While there are tentative signs of a slowdown in activity, with a dip in the number of mortgage approvals for house purchases in June, this has yet to feed through to price growth.

“Demand continues to be supported by strong labour market conditions, where the unemployment rate remains near 50-year lows and with the number of job vacancies close to record highs. At the same time, the limited stock of homes on the market has helped keep upward pressure on house prices.

“We continue to expect the market to slow as pressure on household budgets intensifies in the coming quarters, with inflation set to reach double digits towards the end of the year. Moreover, the Bank of England is widely expected to raise interest rates further, which will also exert a cooling impact on the market if this feeds through to mortgage rates.

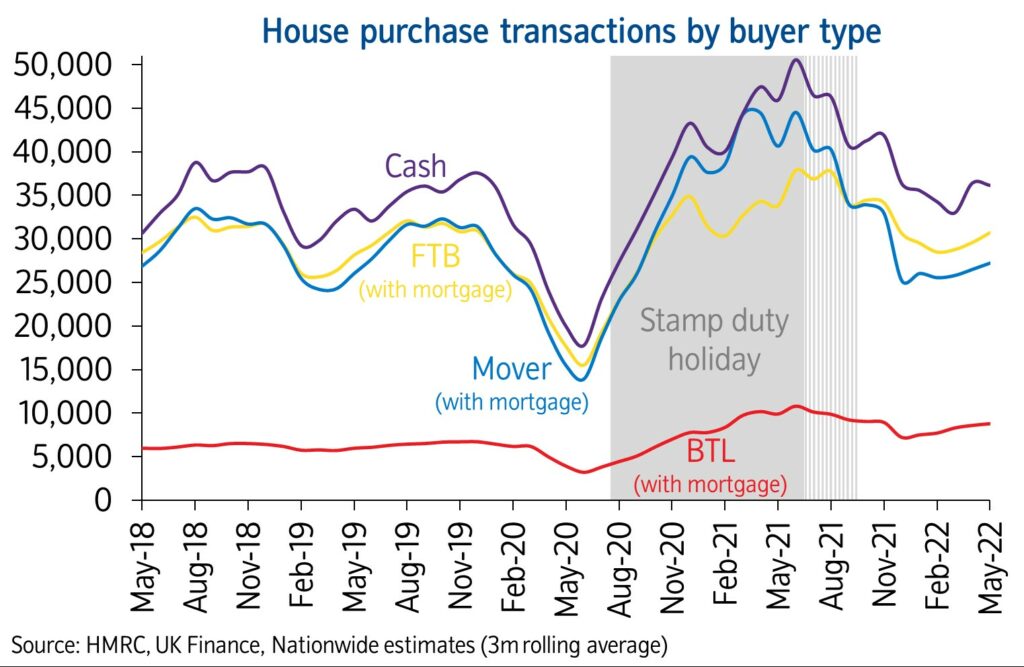

Strength in transactions across buyer types

“Total housing market transactions in the three months to May were c.20% below the elevated levels resulting from the stamp duty holiday, but 5% above pre-pandemic levels.

“Home mover transactions (with a mortgage) have slowed more than other sectors. This probably reflects that the stamp duty holiday had more of an impact encouraging home movers to bring forward purchases, particularly for higher value properties, with no Stamp Duty Land Tax (SDLT) payable up to £500,000 for completions by the end of June 2021. Behavioural shifts due to the pandemic are also likely to have provided more of a boost to home mover activity, where such drivers have now faded.

“First-time buyer mortgage completions have remained resilient, and are now c.5% above pre-pandemic levels, despite growing affordability pressures. Indeed, house price growth has continued to outpace earnings by a wide margin, increasing the deposit hurdle, and, together with higher interest rates, has pushed up mortgage repayments relative to incomes.

“The number of cash transactions has remained elevated, though its share of activity has remained broadly stable at c.35%. This is partly a reflection of an ageing population (where more people own their homes outright). However, properties purchased for investment, such as a holiday home or buy to let, is also an important element of the cash market.

“Buy to let purchases involving a mortgage also remain higher than pre-pandemic levels. Sentiment is likely buoyed by the fact that rental demand remains strong, with upward pressure on rents, which may be encouraging landlords to enter the market, particularly if they view property as a hedge against inflation.”

Give us your thoughts on the future of both mortgage rates and the base rate by taking our short survey here

Reaction

David Reed, operations director of Richmond estate agency Antony Roberts:

“Summer is definitely here and many buyers are away but continued demand for family houses and super apartments is still very much underpinning general sentiment and activity.

“New instructions in coveted areas very much remain a big draw to eager buyers, keen to enquire or set up a viewing. While many families will have secured their desired move prior to the start of the academic year in September, there are still many purchasers looking for an autumn move and are seemingly undeterred by any prospect of a further tweak to interest rates.”

Rose Lyle, director of private clients at property consultants INHOUS:

“We are still seeing very strong demand for good family houses in decent gardens in school catchment areas. Despite stock levels freeing up a little, there is more than one buyer for each house, with competitive bidding on several transactions.

“The autumn market is likely to be strong, despite rising interest rates and worries over the economy. There are plenty of buyers with cash available and, with inflation at the level it is, leaving that money in a bank account does not make sound sense.”

James Briggs, head of personal finance intermediary sales at specialist lender Together:

“House prices increased slightly by 11% in July, once again highlighting the record demand for property in the face of wider economic uncertainty.

“However, due to the impact of the highest levels of inflation in 40 years, cost-of-living challenges and supply shortages, it’s possible that we will soon see the housing bubble start to deflate, particularly in regions that have seen exponential growth in recent years.

“Additionally, the Bank of England may find themselves tightening their monetary policies further to curb inflation with more rate rises afoot, making mortgage borrowing more expensive for buyers and those clients rolling off fixed products.

“With worries of a recession on the horizon, stretched consumers may be reassessing their finances as they brace for autumn, where energy bills are set to soar, and discretionary spending will be increasingly curbed.”

Marc von Grundherr, director of Benham and Reeves:

“You’d have thought that having gorged themselves on a feast of mortgage affordability and stamp duty reductions during the pandemic, the appetite of the nation’s homebuyers would be dwindling.

“This clearly isn’t the case and even a string of consecutive interest rate hikes are yet to taint their taste buds as they continue to pile their plates high – pushing house prices to record highs in the process.

“With the bricks and mortar buffet on offer remaining understocked with regard to the level of homes available, we can expect property prices to remain robust even against an uncertain economic backdrop.”

James Forrester, managing director of Barrows and Forrester:

“A twelfth consecutive monthly increase and yet another double-digit rate of house price growth is quite remarkable in itself, but against the current backdrop of economic uncertainty it really does demonstrate the resilience of UK bricks and mortar.

“Market momentum remains unwavered, having weathered a prolonged period of Brexit uncertainty, a global pandemic, increasing inflation and the most incompetent prime minister in living memory.

“All things considered, it seems as though nothing short of an apocalypse can bring the property market to its knees.”

Geoff Garrett, director of Henry Dannell:

“A combination of rising mortgage rates, inflation and the increased cost of living have already started to cool the property market where buyer appetites in the form of mortgage approvals are concerned.

“Although this is yet to filter through to topline house price growth, it’s inevitable that these headwinds will eventually impact the price buyers are willing to pay.”

Chris Hodgkinson, managing director of HBB Solutions:

“While house prices remain sky high, home sellers would be well advised to fasten their seatbelts as we’re likely to witness a period of heightened turbulence before the year is out.

“Buyer demand levels are already starting to wane and when the well runs dry, home sellers will have to adjust their asking price expectations in order to secure a sale, as a perfect storm of increasing mortgage costs, record inflation levels and the steep cost of living all put pressure on the UK property market.”

Jeremy Leaf, north London estate agent and a former RICS residential chairman:

“The only surprise in these figures is why it is taking so long for the slowdown we have noticed in our offices over the past few months to be reflected in the numbers. But don’t get me wrong – we are seeing a reduction in growth, not a major correction as prices continue to be supported by lack of choice and a strong labour market.

“However, still-rising interest rates and cost-of-living pressures are likely to have an increasing impact in the next few months.”

Tomer Aboody, director of property lender MT Finance:

“Although we are seeing a slight slowdown in growth and transaction levels, buyers are still buoyant and pushing through purchases, although at a more realistic market level. With higher mortgage costs, there are fewer buyers meaning sales on the whole are being transacted at around asking prices rather than multiple offers above, as we have seen previously.

“The slowdown in home movers again suggests that stamp duty needs to be looked at and possibly reviewed, as fewer sellers are looking to move due to high transactional costs.

“It is interesting to see buy-to-let purchases on the rise, as investors take advantage of higher rents, particularly when compared with relatively low returns on bank deposits.

“A slowdown is coming, due to inflation and higher interest rates, but this is likely to be very gradual.”

Iain McKenzie, CEO of The Guild of Property Professionals:

“While house prices continue to defy gravity, the monthly growth figures are starting to level out.

“Demand for properties has dramatically outweighed supply since 2020 and that has pushed prices to record levels.

“Over the past month the number of buyer enquiries has started to subside, and we are seeing a more balanced sales market that could mean we will see house price growth cool.

“While homeowners have seen the value of their property grow substantially, increasing financial pressure from cost-of-living inflation has many hesitant about upscaling and some potential movers are now deciding to stay put.

“When people become hesitant about moving, or their budgets are squeezed too tight and are unable to afford the right home, we could see transactions begin to fall.

“It is unlikely we will see a drop in prices anytime soon. Around half of buyers move because their living situation changes and they are compelled to move to a new property – and so long as this demand remains buoyant, so too will house prices.”

Nicky Stevenson, managing director of national estate agent group Fine & Country:

“Annual house price growth accelerated unexpectedly in July even as storm clouds gathered across the broader economy.

“Increased borrowing costs and shrinking consumer purchasing power have yet to take the heat out of the market, and demand continues to be fuelled by existing homebuyers looking to trade-up.

“Buyers and sellers alike will now be watching closely this week to see if the Bank of England makes good on its threat to hike its base rate to 1.75% — the biggest increase for more than a quarter of a century.

“Cheap debt is fast disappearing and against this backdrop, many expect a period of more subdued house price growth later in the year.”