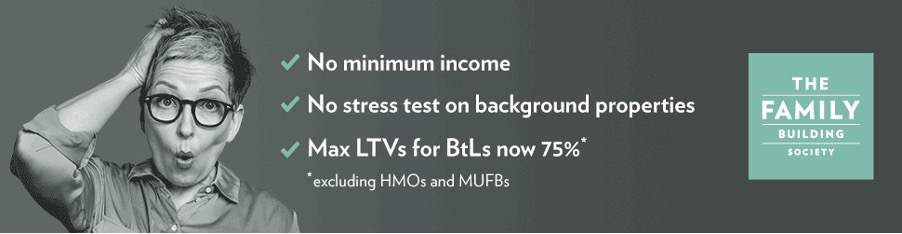

Our criteria can be a bit of an eye-opener. We don’t require the landlord to have a minimum income, we don’t stress test on background properties held and there is no limit to the number of properties in a portfolio. With our manual underwriting approach, we consider each application on a case-by-case basis and make a common-sense decision for your client.

We’re evolving

Buy to Let lending is a significant part of our business. And with around 95% of our business coming through intermediaries, we want to evolve and support our offering to help you to help your clients.

We know that with rising interest rates, increased regulation, and the approaching Renters’ Rights Bill, landlords face a more challenging and complex landscape than ever before.

We’ve taken a strategic step forward to improve our Buy to Let criteria aligning with broader market trends and providing additional support to landlords in an uncertain market. We recently increased our Loan to Value to 75%, up from 70%, across our standard Buy to Let product range, (LTV remains at 70% for HMO and MUFBs).

In recent years, houses in multiple occupation (HMOs) have gained significant traction in the rental market, reflecting evolving tenant demand and the increase in professional landlords wanting to diversify. In February this year, we launched a HMO offering – currently available through selected packagers and we’ll be widening this to general sale from Monday 24 March. This is a natural progression in our journey, establishing our strong position in the market.

How can we help?

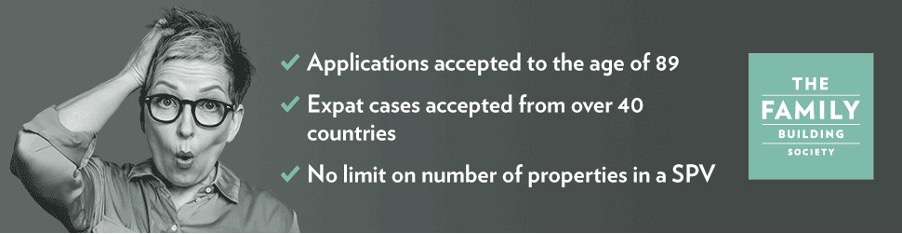

In line with our mission to provide support landlords whether they’re large or small, our criteria is intentionally flexible. There’s no minimum income requirement or stress test on background properties held (only self-financing properties required). We’ll accept expat cases from over 40 countries, including more through agreed packagers. We also have very generous terms when it comes to age and accept applications up to the age of 89 – a major differentiator that extends the helping hand to a wide range of clients.

Our team of BDMs cover the whole of the UK so brokers always have a personal contact they can speak to. The close relationship between our BDMs and underwriting team is so important when dealing with complex cases, as applications can be discussed before submission. If a BDM can’t agree a case straightaway, they can discuss it with an underwriter who potentially may be able to agree an exception. This speeds up the process and adds a human touch which mainstream lenders are unable to offer.

A reminder of our criteria

- No stress test on background properties held (only self-financing properties required)

- Max LTV for BtL products now 75%, excluding HMOs and MUFBs which remain at 70%

- We accept applications up to the age of 89

- Expat cases accepted from over 40 countries, plus more through agreed packagers

- HMO products for up to 4 bedrooms now available through selected packagers – speak to your local BDM to find to more

- We have a common-sense approach to lending and use real human beings to underwrite each mortgage case.

This is how we, at Family Building Society, underwrite our mortgages. Case by case, story by story – catering for accidental landlords with one or two properties, to professional landlords with large portfolios. We take great pride in the how we do things, and it works.

To contact our Mortgage Desk or your local BDM,

CALL US ON: 01372 744155

OR EMAIL: mortgage.desk@familybsoc.co.uk

| FAMILY BUILDING SOCIETY, EBBISHAM HOUSE, 30 CHURCH ST, EPSOM, SURREY KT17 4NL Family Building Society is a trading name of National Counties Building Society which is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. National Counties is on the Financial Services Register Firm Reference Number 206080. |