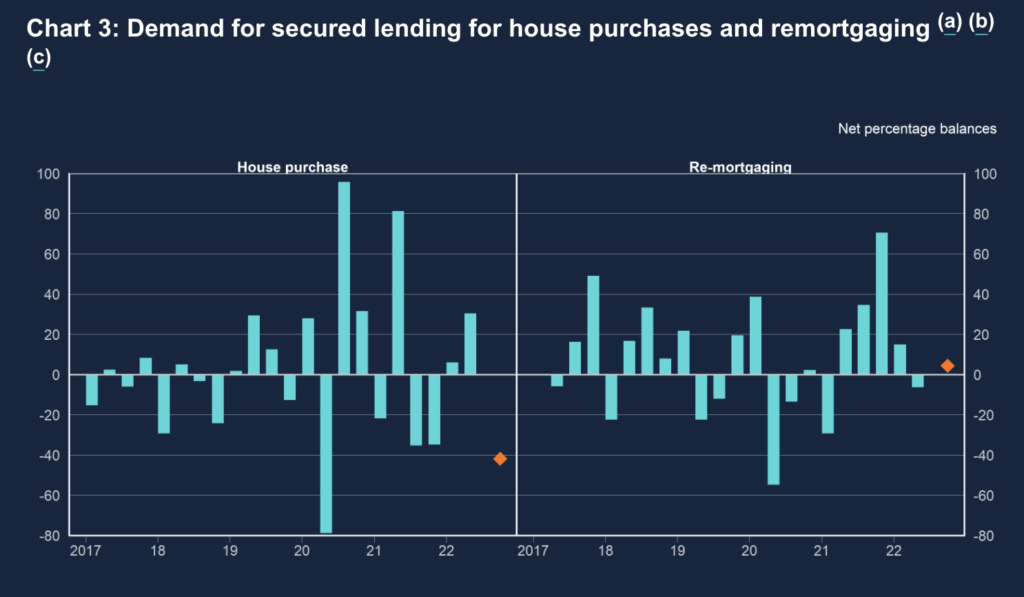

Lenders reported that demand for mortgage lending increased in Q2, but they expect it to drop in Q3. That’s according to the Bank of England’s credit condition report.

Surprisingly demand for remortgaging slightly decreased in Q2, and was expected to be unchanged in Q3.

The net percentage balance for changes in default rates on secured loans to households slightly decreased in Q2, and was expected to increase in Q3.

While the net percentage balance for changes in losses given default on secured loans decreased in Q2, and was expected to be unchanged in Q3.

Demand for lending on credit cards and loans rose between April and June, and demand for cards is expected to do so again through the summer, as rising prices take their toll.

Reaction

Sarah Coles, senior personal finance analyst, Hargreaves Lansdown:

“Demand for debt flourished this spring, as price rises ran rampant. The banks expect us to keep reaching for our credit cards to plug the growing gaps in our finances during the summer too.

“Unfortunately, it means people risk building up even bigger problems further down the track, which is one reason why the banks are toughening up.

This was the period when the energy price cap hiked kicked in, and we felt price rises most keenly. The HL Savings and Resilience Barometer found that as a result of price rises across the board, real disposable income fell by 3%, so 41% of households were forced either to cut their costs, dip into savings or borrow money. This data shows that borrowing has been a key part of this picture.

So far, lenders have been keen to make this borrowing available, but over the summer, they’re planning to tighten the purse strings. With inflation at this level, they’re mindful that there’s a rising risk that people will struggle to stay on top of their debts.

The problem with borrowing for everyday costs is that you’re adding more interest and repayments to your ongoing costs, so that every month, the impossible challenge of making ends meet becomes harder. As we’ve gone through the year, rising interest rates have added to the problem.

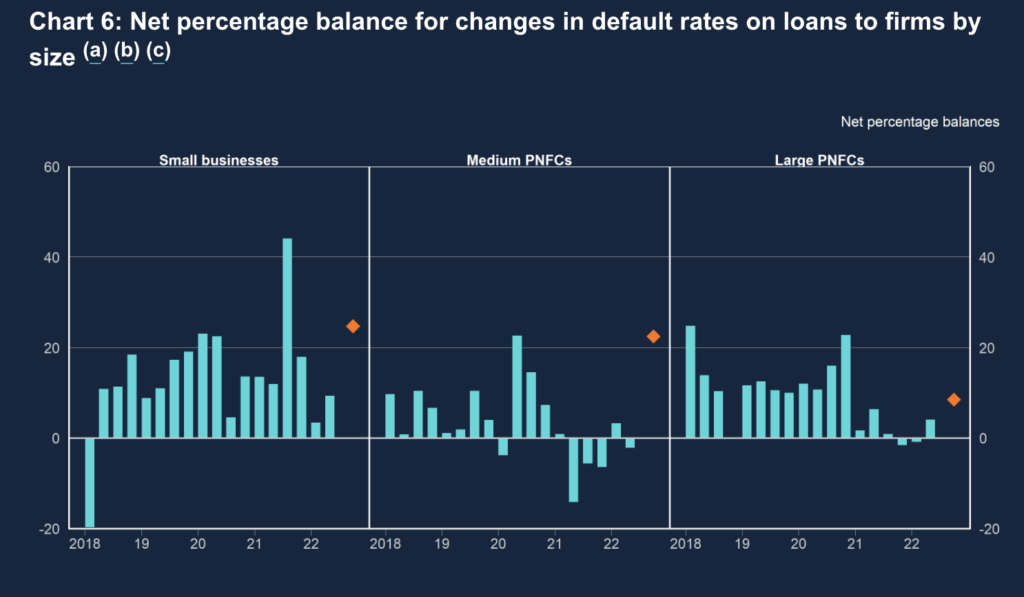

It’s no wonder that defaults on unsecured lending increased over the spring, and the banks say they’re expecting default rates on both mortgages and unsecured lending to rise in the next couple of months.

It got tougher to secure a mortgage during these three months, as banks started factoring higher prices into their mortgage calculations.

“They said they expected to make it even harder to borrow over the summer. It’s yet another pressure on the housing market, which is showing signs that it’s starting to cool. And while demand for mortgages increased during the spring, the banks are expecting this to fall away a little over the coming months.”

Mark Harris, chief executive of mortgage broker SPF Private Clients:

“Continued strong activity in the housing market is reflected in these figures with demand for mortgages increasing in the second quarter, although this is expected to decrease in the third quarter as the froth continues to come out of the market.

“Remortgaging activity slightly decreased, which is surprising as many borrowers have been keen to secure fixed rates in the face of rising interest rates.

“Spreads narrowed slightly as lenders absorbed some of the rising cost of borrowing. However, lenders reported that these are expected to widen in the third quarter as mortgage rates continue to rise.”

Jeremy Leaf, north London estate agent and a former RICS residential chairman:

“Just like the UK economy, the housing market continues to defy expectations.

“Still unsatisfied demand is shrugging off concerns about the cost of living and rising interest rates. But we know, on the ground, that the market is changing as transactions are reducing and lengthening. Lack of choice is continuing to underpin pricing.”